Forter

Founded Year

2013Stage

Series F | AliveTotal Raised

$525MValuation

$0000Last Raised

$300M | 3 yrs agoMosaic Score The Mosaic Score is an algorithm that measures the overall financial health and market potential of private companies.

-30 points in the past 30 days

About Forter

Forter focuses on fraud prevention and protection in the digital commerce industry. The company offers services such as fraud management, payment optimization, chargeback recovery, identity protection, and abuse prevention, all aimed at increasing revenue, reducing losses, and enhancing the customer experience. It primarily serves the digital commerce industry. It was founded in 2013 and is based in New York, New York.

Loading...

Forter's Product Videos

ESPs containing Forter

The ESP matrix leverages data and analyst insight to identify and rank leading companies in a given technology landscape.

The payments fraud detection & prevention market offers a range of technologies helping businesses detect and block anomalous payment activity. Vendors in this market cater to many different industries, from financial services to e-commerce. These solutions cover a range of different types of financial fraud like chargebacks, ACH, wire, and credit card fraud.

Forter named as Challenger among 15 other companies, including Mastercard, Oracle, and Fiserv.

Forter's Products & Differentiators

Forter Payment Protection

Forter’s Payment Protection platform provides accurate, real-time decisions for every transaction -- allowing more good buyers to make purchases while keeping fraud out. The Payment Protection platform includes solutions to help merchants deal with transaction fraud, phone fraud, and omnichannel fraud. Additionally, the platform offers solutions to help with PSD2 protection, Forter’s Trusted Authorization solution to connect merchants directly with issuing banks, and Forter’s 100% chargeback guarantee to erase chargeback costs from a merchant’s bottom line.

Loading...

Research containing Forter

Get data-driven expert analysis from the CB Insights Intelligence Unit.

CB Insights Intelligence Analysts have mentioned Forter in 10 CB Insights research briefs, most recently on Mar 18, 2024.

Mar 14, 2024

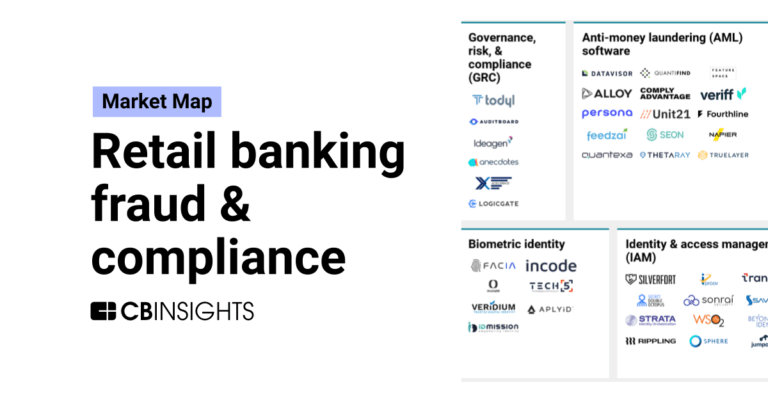

The retail banking fraud & compliance market map

Feb 27, 2023 report

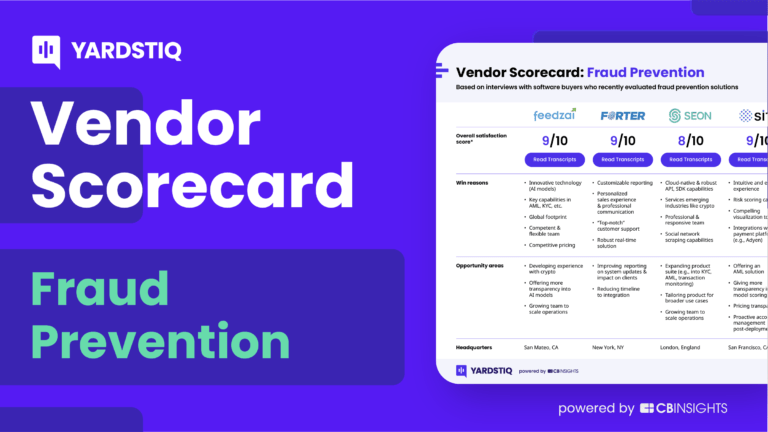

Top fraud prevention companies — and why customers chose them

Apr 19, 2022 report

Why payments leaders are prioritizing fraud preventionExpert Collections containing Forter

Expert Collections are analyst-curated lists that highlight the companies you need to know in the most important technology spaces.

Forter is included in 10 Expert Collections, including E-Commerce.

E-Commerce

11,250 items

Companies that sell goods online (B2C), or enable the selling of goods online via tech solutions (B2B).

Unicorns- Billion Dollar Startups

1,244 items

Payments

3,033 items

Companies in this collection provide technology that enables consumers and businesses to pay, collect, automate, and settle transfers of currency, both online and at the physical point-of-sale.

Fintech 100

999 items

250 of the most promising private companies applying a mix of software and technology to transform the financial services industry.

Tech IPO Pipeline

825 items

Conference Exhibitors

5,302 items

Forter Patents

Forter has filed 3 patents.

The 3 most popular patent topics include:

- online payments

- payment service providers

- payment systems

Application Date | Grant Date | Title | Related Topics | Status |

|---|---|---|---|---|

1/8/2016 | 8/1/2017 | Rules of inference, Data management, Information technology management, Transaction processing, Internet culture | Grant |

Application Date | 1/8/2016 |

|---|---|

Grant Date | 8/1/2017 |

Title | |

Related Topics | Rules of inference, Data management, Information technology management, Transaction processing, Internet culture |

Status | Grant |

Latest Forter News

Sep 4, 2024

undefined mins Adam Davies, VP of Product Management at FICO, discusses the critical role of real-time fraud detection and AI in staying ahead of emerging threats in the fintech sector. Today, AI has given fraudsters new tools for malicious ends. We look at what FIs can do to stay at the cutting edge of cybersecurity innovation Today, fraud is among the leading pain points for financial services institutions and consumers alike. As new AI-driving technologies help drive innovation in the sector, so too do they give fraudsters the tools to carry out their malicious aims. In this roundtable, we speak to industry experts on ways fintechs can stay at the cutting edge of cybersecurity innovation amid rampant, rising fraud rates. Fraud rate increases, UK Finance: UK Finance reported £1.2bn losses through payments fraud in 2023. In 2023, UK Finance sent out 427 fraud-related alerts to the industry, disseminating over 2 million compromised card numbers. Over 2.9 million cases of fraud were reported in totla in the UK in 2023. Our speakers: Grigory Yusupov, Regional Director UK and Rest of the World (ROW) at IDnow Doriel Abrahams, Principal Technologist at Forter How important is it for fintechs to stay at the cutting edge of cybersecurity innovation, using AI to stay one step ahead of fraudsters? How can they do it, and what more needs to be done? Adam Davies: Banks and fintechs are locked in a race against the fraudsters, a race that’s moving more quickly every day. Fraudsters are using new technologies like Generative AI to increase the speed of their attacks, defeat authentication and socially engineer/scam customers at a scale we’ve never seen before. Fintechs have to match that speed and make fraud decisions increasingly quickly, with real-time decisions becoming table stakes to stay ahead of criminals. Fintechs also need to use all the available data to identify anomalous behaviour that might indicate fraud. Whether they’re extracting context from internal data, or bringing in external data, all those relevant signals can help make an informed decision about whether something is fraudulent or legitimate. Finally, fintechs need the agility to react as fraud types and channels change. Using technology that allows nimble orchestration and the rapid modification and deployment of new fraud-fighting strategies is essential given the very dynamic nature of fraud threats. Relying on static rules or offline detection will only make a fintech a target for sophisticated fraudsters. Grigory Yusupov: We are already witnessing how developments within Artificial Intelligence (AI) are having some adverse effects on cybersecurity. The extraordinary leaps in AI technology mean it’s now almost too easy for a fraudster to carry out financial crimes. As AI develops further, social engineering attacks on organisations will become easier and faster because cybercriminals no longer need deep technical know-how to execute them. Particularly, advancements in generative AI mean deepfake technology can now be used to create hyper-realistic fake documents and videos used to commit financial crimes and fraud. The frightening accuracy of deepfakes means that document forgery is likely to become easier than ever before, with accurate information harder to spot by the naked eye. To combat these AI-aided advances of cybercriminals, organisations will need to fight fire with fire by leveraging AI themselves to stay one step ahead. Doriel Abrahams: Staying ahead in cybersecurity is crucial for fintechs as fraudsters increasingly use AI for sophisticated attacks. It’s important to remember that AI is not a good fraud instigator, it’s a great fraud accelerator and fraudsters can now automate and scale large portions of their operations. To best combat it, fintech organisations should leverage AI technologies to detect and respond to threats in real-time, using behavioural analytics and focusing on the persona, and the user’s identity, rather than easily manipulated attributes such as billing or IP addresses. Continuous innovation, collaboration with industry peers, and investment in R&D are essential to maintain security and build trust. Grigory Yusupov, Regional Director at IDnow, explores how advancements in AI and deepfake technology are reshaping the landscape of cybersecurity and fraud prevention. How can finservs/fintechs ensure the customer is secure against potential fraud, not just from a technological standpoint, but in educating the customer about potential dangers as well? Adam Davies: Protecting customers is absolutely at the convergence of technology and education. Fintechs can actually get the customers involved in the fraud detection process, which helps the customer feel protected and empowered while building trust with the company. By using technology to engage customers consistently, fintechs can make sure that they are balancing friction with convenience. Engaging customers in their preferred channels (whether SMS, fintech app, phone call, email, etc) and giving them the option to self-resolve something like a monetary transaction, helps reinforce the fintech’s role as the protector of their accounts and trusted advisor. But it’s not just about that one moment or single transaction. Ongoing education efforts should also be a part of the fintech’s strategy, and companies can use omni-channel communication capabilities to share tips, tricks and knowledge to help consumers protect themselves against emerging or evolving fraud threats. Especially with the increase in scams, banks need to get customers to “stop and think” which might be needed to break the spell the scammers have over the customer. Grigory Yusupov: The speed and scale at which AI can enable cybercrime is a thing to behold. With limited skills, nefarious individuals and groups can now target fintech organisations and their customers with relative ease. Collaboration is critical, as technology alone cannot eradicate fraud. In fact, there is no silver bullet for fighting fraud; it is something that manifests at every online touchpoint, affecting individuals and organisations equally. The key will be to work together to identify the forms of AI-enabled cybercrime and devise ways to combat them through technology and education. According to the IDnow UK Fraud Awareness Report 2024, 33% of Brits have shared scans or photos of an ID card, driving licence or passport via insecure digital channels, such as social media or email, despite knowing that these ID documents could land in the wrong hands. However, less than a third (31%) of Britons know what deepfake documents are, nor are they aware of the potential risks posed by digitally generated images of physical documents. The public must be educated on the threats associated with sharing highly sensitive personal information online. Our advice is always to think twice before sending a scan or photo of official ID documents into the digital ether via unencrypted channels. Alongside deepfakes and document forgery, another risk that stems from AI is social engineering, which, unlike other forms of cyberattacks, appeals to human vulnerabilities and emotions. In these cases, generative AI may be used by criminals to target exposed people within organisations, to elicit information or make a financial gain. Doriel Abrahams: Fintechs must combine classic advanced security measures like multi-factor authentication and encryption with customer education: regular awareness campaigns, phishing alerts and training resources help customers recognise and avoid fraud. Open communication channels ensure customers feel supported and informed. Blockchain and DLT (distributed ledger technology) can mitigate fraud by creating immutable ledger transactions. How is it being employed today, and what are the barriers to organisations that currently aren’t leveraging blockchain technology? Adam Davies: Fintechs and other companies in financial services are always looking to understand the value that new technologies like blockchain (distributed ledger technology) can provide. At FICO, we have pioneered a technique for blockchain/distributed ledger technology to improve model governance and observability. We were recently awarded a patent for the use of blockchain technology to track the end-to-end provenance of the development, operationalisation and monitoring of machine learning models. This allows us to offer explainability to all our customers and promote explainability in all our transactional fraud models and model development. Grigory Yusupov: In financial services, blockchain can be used to increase the security and transparency of transactions. As an example, banks can use blockchain to streamline cross-border payments and reduce fraud through an unambiguous, immutable record of each transaction. However, today’s adoption of blockchain and DLT is still often hindered by technical, regulatory, cost, and organisational barriers. One example of the regulatory challenges associated with blockchain and DLT is the new Transfer of Funds Regulation (TFR) in the EU, which mandates that all cryptocurrency transactions will need to carry identifying data of the sender and the receiver. According to the new rule, compliance with TFR is mandatory for all Crypto Asset Service Providers (CASPs). One challenge for CASPs lies in GDPR compliance, as personally identifiable information (PII) should not be stored on blockchains or DLT. However, to comply with the new regulations, CASPs need to know with whom they are doing business and continuously verify this information. Doriel Abrahams, Principal Technologist at Forter, highlights the critical role of AI and continuous innovation in staying ahead of sophisticated fraud threats in the fintech sector. Today, finance fraud is happening beyond the KYC stage. How can fintechs/finserv enhance their onboarding processes and ensure fraud beyond the KYC stage is limited? Doriel Abrahams: Doriel offers three key points for FIs to take note of during the onboarding and KYC processes to reduce fraud. Continuous, real-time monitoring: Monitor customer transactions and behaviour for signs of fraud even after the initial KYC process. Behavioural Analysis: Utilising behavioural data points to monitor how users interact with the platform, detecting and flagging unusual behaviours. Dynamic KYC: Implementing dynamic KYC processes that periodically re-verify customer identities and update their risk profiles. This is important not only to stop fraud but also to generate trust with good users who deserve less friction in the user experience. Adam Davies: Accessing data from across multiple internal and external systems (eg, device intelligence, biometric validation, contact data verification) will help to resolve customers' identities and transform that data to the appropriate format for making decisions. That level of insight also helps put the customer's interaction in a historical context, which can enable fintechs to identify anomalies that may indicate fraud. Link analysis/social network analysis helps to associate data entities and perform data matching across multiple data sources, such as applications and account records. Matching can uncover links indicative of criminal activity, and connections that are several degrees separate can be detected and visualised. Finally, fintechs need dynamic orchestration to meet the requirements of each specific scenario, whether during the onboarding process or during a customer management process. For example, the source of an application helps to determine what identity checks are invoked; or a high-value transaction to a new beneficiary may result in more stringent identity verification than a small dollar transaction to a known beneficiary. That level of agility and composability allows fintechs to deliver truly personalised experiences that help reduce fraud while meeting customer expectations. Grigory Yusupov: As financial fraud happens beyond the KYC stage, fintechs should implement an effective, long-term cybercrime and fraud prevention strategy. So-called risk signals are an innovation within the added ‘layers of defence’ that fintechs can use to tackle cybercrime after the initial KYC process is complete. In fact, more focus will have to be placed on authentication processes rather than focusing only on the initial verification process of a user. In the future, users will likely have to prove their identity through authentication measures throughout their user life cycle. Fintechs and financial service providers will be able to mitigate risks by adding an extra layer of authentication. To read the full story in the magazine click HERE ************** Make sure you check out the latest edition of FinTech Magazine and also sign up to our global conference series - FinTech LIVE 2024 **************

Forter Frequently Asked Questions (FAQ)

When was Forter founded?

Forter was founded in 2013.

Where is Forter's headquarters?

Forter's headquarters is located at 575 Fifth Avenue, New York.

What is Forter's latest funding round?

Forter's latest funding round is Series F.

How much did Forter raise?

Forter raised a total of $525M.

Who are the investors of Forter?

Investors of Forter include Scale Venture Partners, NewView Capital, March Capital, Salesforce Ventures, Sequoia Capital and 17 more.

Who are Forter's competitors?

Competitors of Forter include Resistant AI, Fraud.net, Vesta, Nethone, FUGU and 7 more.

What products does Forter offer?

Forter's products include Forter Payment Protection and 4 more.

Who are Forter's customers?

Customers of Forter include TAG Heuer, SNIPES, Priceline, Delivery.com and Nordstrom.

Loading...

Compare Forter to Competitors

Sift provides real-time machine learning fraud prevention solutions for online businesses. Its machine-learning software automatically learns and detects fraudulent behavioral patterns and alerts businesses before they or their customers are defrauded. It provides its services in a wide range of industries such as financial technology, retail, payment service providers, and more. It was formerly known as Sift Science. It was founded in 2011 and is based in San Francisco, California.

Signifyd provides e-commerce fraud protection and prevention services. The company offers services, including revenue protection, abuse prevention, and payment compliance, all aimed at maximizing conversion and eliminating fraud and consumer abuse. These services primarily cater to the e-commerce industry. Signifyd was founded in 2011 and is based in San Jose, California.

Ravelin specializes in fraud prevention and payment security within the online business sector. The company offers a suite of solutions that utilize machine learning and human insights aiming to protect against online payment fraud, account takeovers, policy abuse, marketplace fraud, and optimization of three-dimensional secure transactions. Ravelin primarily serves online merchants looking to secure their transactions and enhance customer journey. It was founded in 2014 and is based in London, United Kingdom.

Shield is a device-first risk AI platform specializing in fraud prevention and risk intelligence within the digital business sector. The company offers solutions to identify and eliminate fraudulent activities through global standard device identification and actionable risk intelligence. Shield primarily serves industries such as ride-hailing, social media, e-commerce, digital banking, and gaming. Shield was formerly known as CashShield. It was founded in 2008 and is based in Singapore, Singapore.

BioCatch is a company specializing in behavioral biometrics for fraud prevention and digital identity verification within the financial services sector. The company offers solutions that analyze online user behavior to detect and prevent fraud, money laundering, and various cyber threats. It was founded in 2011 and is based in Tel Aviv, Israel.

NS8 is an eCommerce company that provides abuse, fraud, and user experience protection tools. The company uses behavioral analytics, real-time user scoring, and global monitoring to optimize and protect against threats, which give eCommerce merchants insight into their real customers.

Loading...