Data shows private market players are more highly valued than their public market counterparts despite dramatically less revenue. Primary intel gathered from interviews with software buyers reveals a mixed bag on CSAT, features, and pricing across vendors in the space.

The collaboration & project management software market is becoming increasingly crowded.

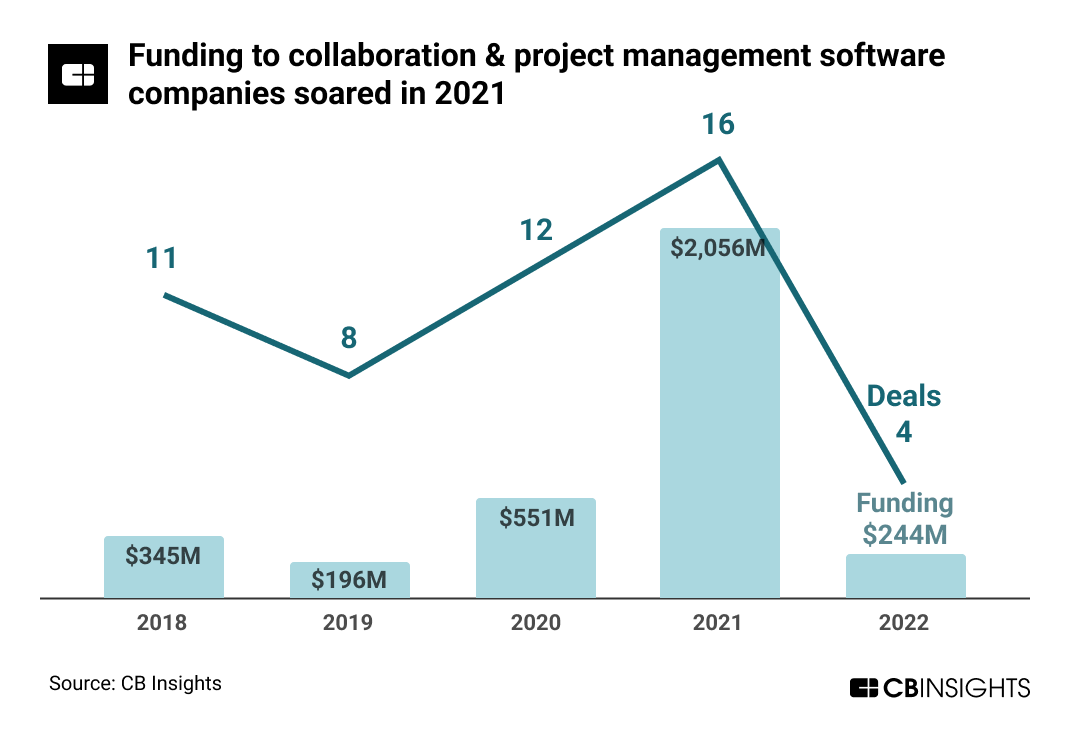

In 2021, these companies — which help teams communicate, collaborate, and manage projects more efficiently — collectively raised $2B+ in equity funding. 2021 also saw the exits of Monday.com (went public at a $5.8B valuation) and Wrike (acquired for $2.3B).

In 2022, against the backdrop of the larger venture market pullback, deal activity to collaboration & project management vendors dropped dramatically. Part of this was likely a function of the amount of capital raised in 2021 — most companies raised warchests at lofty multiples, eliminating a need for more capital in 2022.

In 2022, against the backdrop of the larger venture market pullback, deal activity to collaboration & project management vendors dropped dramatically. Part of this was likely a function of the amount of capital raised in 2021 — most companies raised warchests at lofty multiples, eliminating a need for more capital in 2022.

Now, public and private players alike are jockeying for revenue growth (and profitability) amid rising competition in the space.

In this market analysis report, we’ll dig into:

- What are the top collaboration & project management software vendors?

- What are the 5 primary challenges that buyers/users face with these solutions?

- What are software buyers saying about collaboration & project management software vendors?

- Market stats: How do key collaboration & project management software vendors compare across funding, valuation, revenue multiples, and other efficiency stats?

What are the top collaboration & project management software vendors?

Notable collaboration & project management software vendors include:

Ten of the players listed above have public or private market valuations of $1B+ (more on the valuations below).

Monday.com, Asana, and Smartsheet are all publicly traded. Trello (acquired by Atlassian for $425M), Wrike (acquired by Citrix for $2.3B), and Planview (acquired by TA Associates and TPG Capital) are no longer standalone companies.

What are the 5 biggest challenges that buyers/users face with these solutions?

Through Yardstiq, analysts regularly speak with buyers of collaboration & project management (C&PM) software solutions. Below are the 5 common challenges we’ve heard they face in their adoption of these solutions.

- User adoption: Getting team members to use the new software is a challenge especially in the face of existing habits. Training and support is critical.

- Integration with existing systems: Success often requires integration with other tools and systems, i.e., email, CRM, and HRIS. This can be complex and time-consuming.

- Data migration: Migrating data and info from one solution to a new C&PM solution is a time-consuming and error-prone process. As a result, companies often have multiple tools.

- Customization: Certain workflows within companies require customization. Some products are limited here and getting technical resources to create these workflows is challenging.

- Ongoing maintenance and support: Keeping C&PM solutions clean and usable requires dedicated time and resources.

What are software buyers saying about specific collaboration & project management software vendors?

Conversations with customers of these collaboration & project management software also reveal first-hand areas of opportunity, competitive advantages, strengths, and more.

Below are some quotes from Yardstiq.

Customers with access to Yardstiq can click on the links below to read the full transcript.

Asana customer (CSAT: 9)

I work on top of Asana every day. I’m a very heavy user…For me, the main weakness is that they don’t have timekeeping. For us, it is very hard. They recommended a horrible platform they have that is hyper-expensive that is called Harvest. It’s a timekeeping associate of Asana. We tried it but it’s incredibly expensive and then we end up using Everhour that integrates very well with Asana, but I would love not to have an integration, but native billing timekeeping. At the beginning, we planned to leave Asana because we needed timekeeping, but at the end, this Everhour came up, and we stayed with Asana. — Manager, Data Analytics at Consulting firm

Asana customer (CSAT: 9)

I think at the end of the day, it really came down between Wrike and Asana, just because a company we acquired was using Wrike, and so it was already culturally embedded. And so that’s where we had to sit down and figure out what makes sense in the long term here. Asana had more integrations. It was already heavily integrated into our security suite and things like that. The features that they needed out of the competitor was already available in Asana and working really well. So we were able to do a pretty straightforward transition into Asana. — Director, IT Infrastructure at Media company

Smartsheet customer (CSAT: 8)

So, I don’t know if you’ve ever actually played with the tool, but something that’s interesting is when you are building those dashboards, it’s not simple to update them. Once they’re built, they’re beautiful, but to update them is very complex because you have to move each item to make room for a new item, if that makes sense. So, even though it’s customizable, it’s a big challenge. And I like how they were open about that. And then the other thing I liked about it is the roadmap. We’re using a lot of features today…there is a whole conversation about what’s next, what’s on the roadmap. — Head of Automation, $10B+ market cap software company

Smartsheet customer (CSAT: 5)

I’ll be honest, we’re not renewing them. We’re ending our services with them at the end of the year, because we decided to build an in-house tool. This was like inflation and every year their price is just drastically increasing, we had to eventually say enough is enough type of thing. — Director, Customer Experience at Fortune 500 company

Productboard customer (CSAT: 8.5)

So we already use Jira. Productboard was not going to replace Jira. So that’s a key thing to call out. Some internal people wanted us to use the Jira roadmap feature, which really falls short of what Productboard can do. So the best way to describe it is Jira is the execution tool for developers. Productboard sits ahead of Jira, one step ahead, and it’s the planning tool for product managers….

We looked at Aha!, which I’ve used in the past, which is overly complex. And I had a really bad experience using that with the team in the past, so we did not want to use that. And then there’s other things like a Trello or something, which are just using a Kanban board for something that it’s not intended for and it’s not mature enough of a tool. I think it’s great for what it does, but it doesn’t build road maps and help you make priority decisions. It just documents whatever you put in it. — Head of Product Management at $100M+ funded consumer products company

Market stats: How do key collaboration & project management software vendors compare across funding, valuation, revenue multiples, and other efficiency stats?

Across the top 10 players in the space, below are comparisons and graphs analyzing their:

- Funding

- Valuations

- Revenues

- Revenue multiples (price to sales)

- Revenue:funding efficiency ratios

- Funding:valuation ratios

Funding comparison

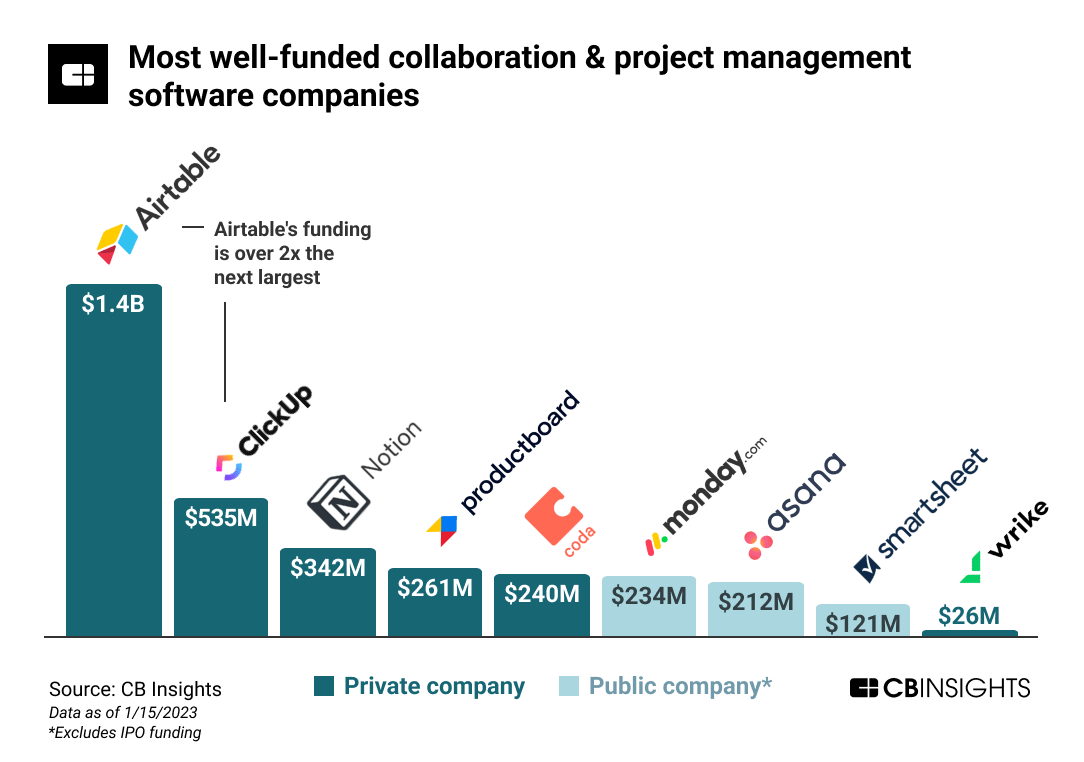

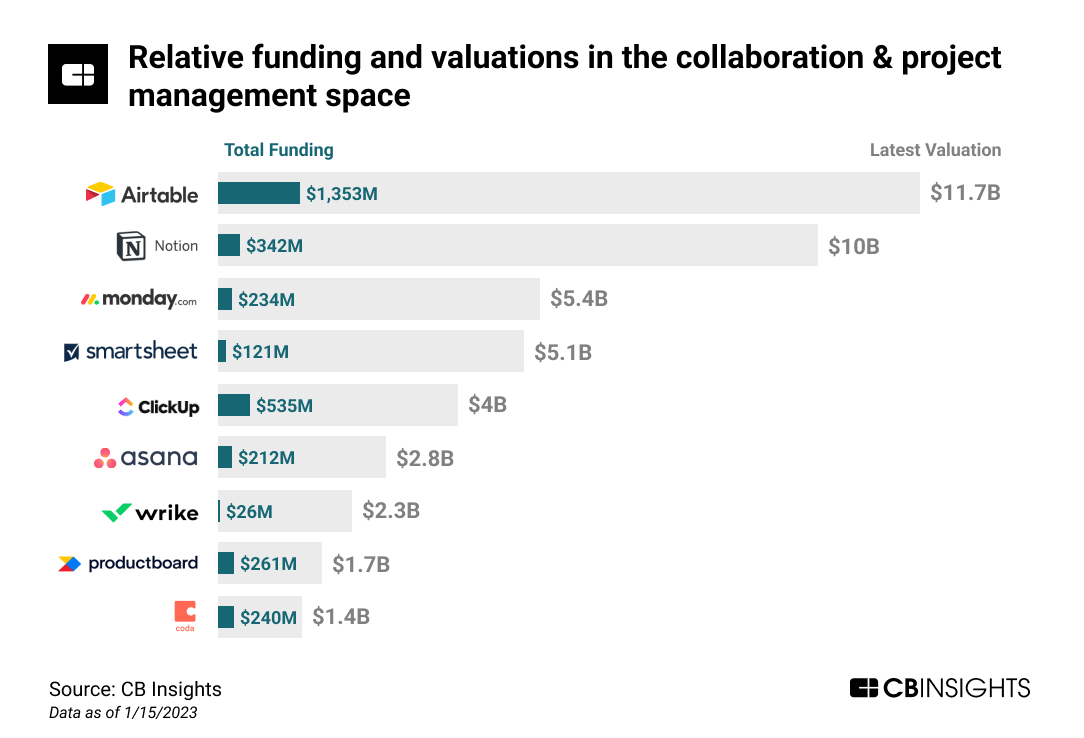

- The funding activity shown earlier has largely been driven by mega-rounds ($100M+ deals) to the unicorns in the space, as the massive financings raised by the companies below highlight.

- Current, non-exited private players in collaboration & project management have raised dramatically more than their now-public peers had raised prior to going public.

- Airtable has raised 2.6x its next most well-funded competitor.

Valuation comparison

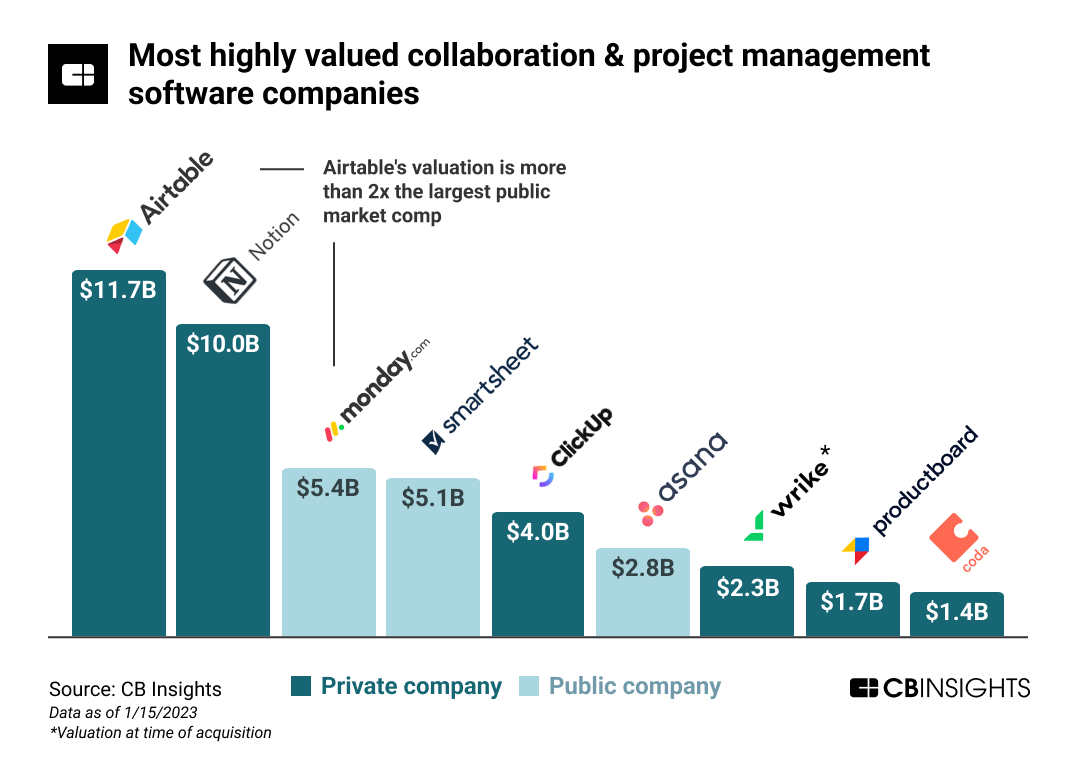

- Similar to funding, private market valuations are dramatically higher than public peers.

- In this case, the valuations of Airtable and Notion are nearly double those of Monday.com and Smartsheet and more than 3x Asana’s.

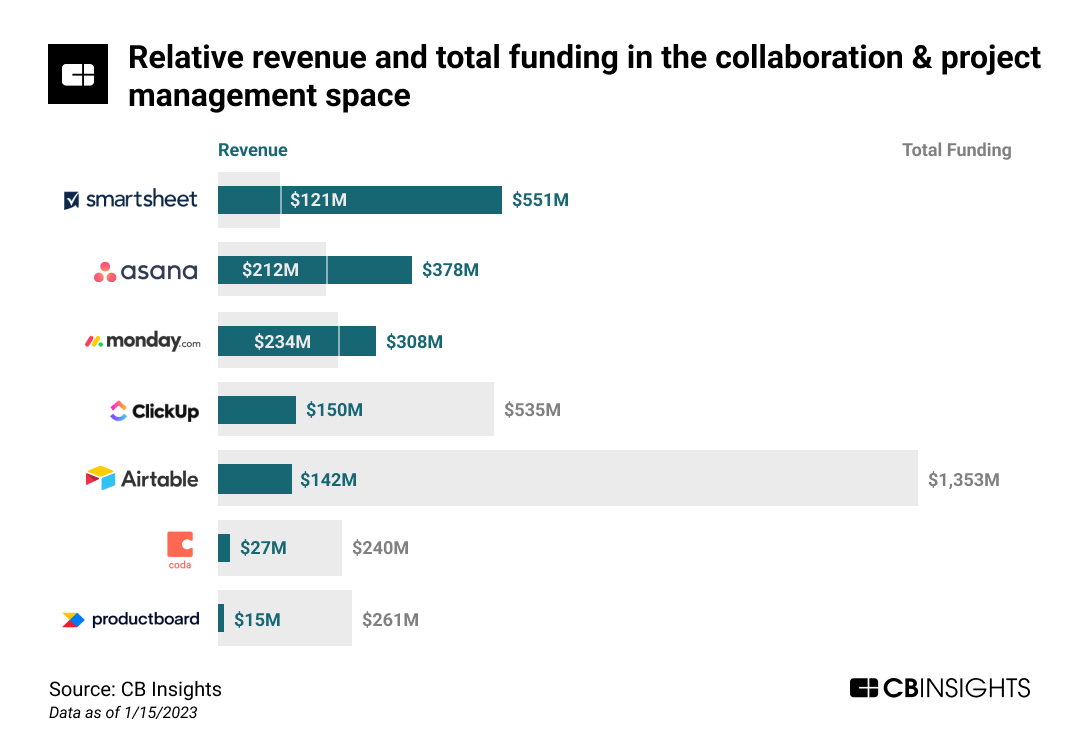

Revenue comparison

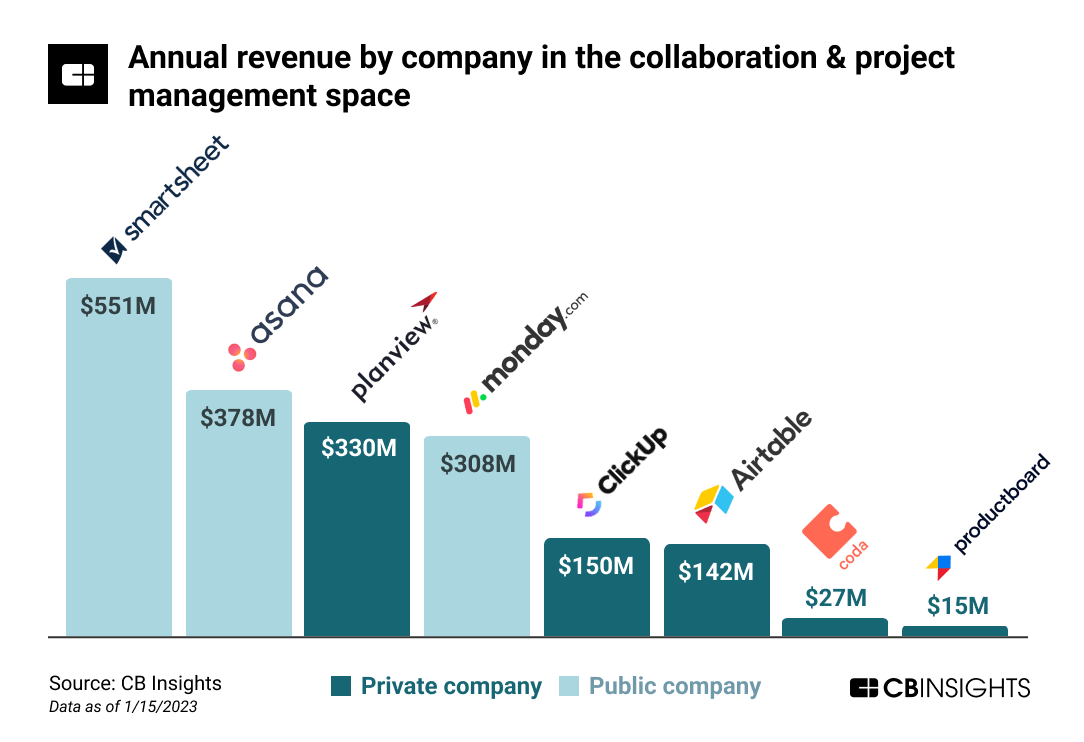

- Although private market players have higher funding raised and valuations, the public players in collaboration & project management software have dramatically higher reported revenues.

- Smartsheet has 3.87x the amount of revenue as Airtable, but Airtable’s valuation is 2.29x Smartsheet’s.

Revenue multiple comparison

- The median and average price/revenue valuation multiple (in other words, valuation divided by revenue) of public players in the space are 9.3x and 11.4x, respectively.

- Privately held players by comparison have a median and average multiple of 51.3x and 56.5x, respectively.

- Productboard has the loftiest valuation multiple of 117.4x. Airtable, which leads in total funding, also has a lofty valuation multiple of 82.4x.

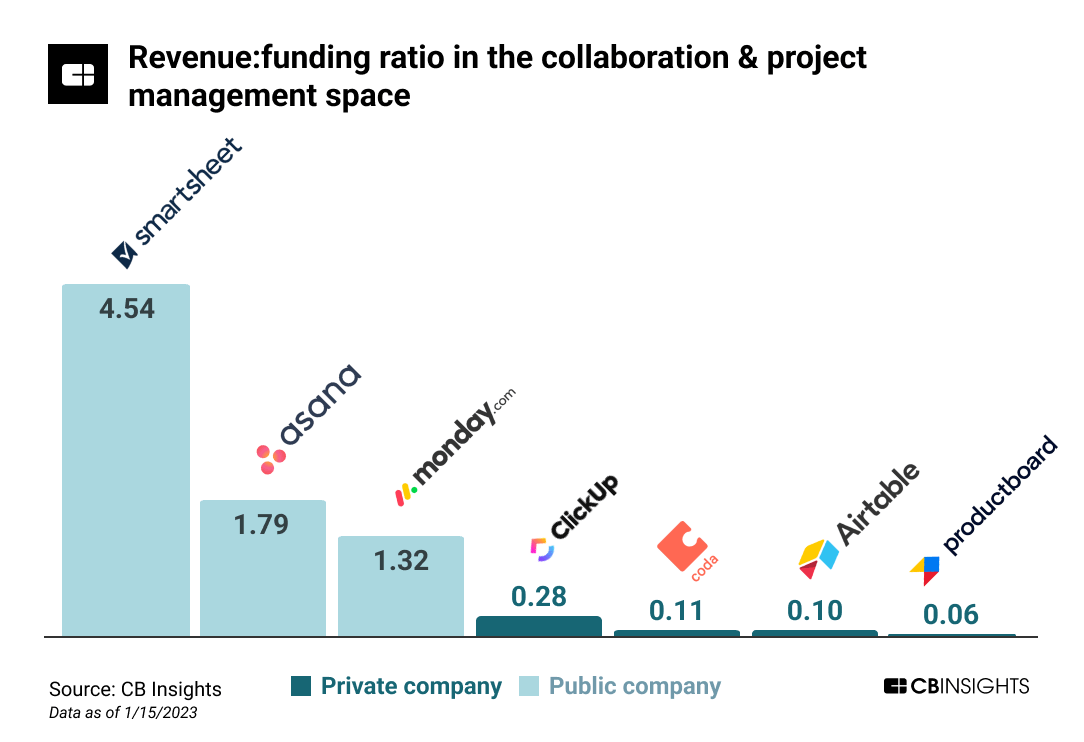

Revenue to funding comparison

- The ratio of revenue to funding (revenue:funding) highlights how well companies have been able to turn funding into revenue.

- The dichotomy between public and private players is very obvious as the graphs below illustrate.

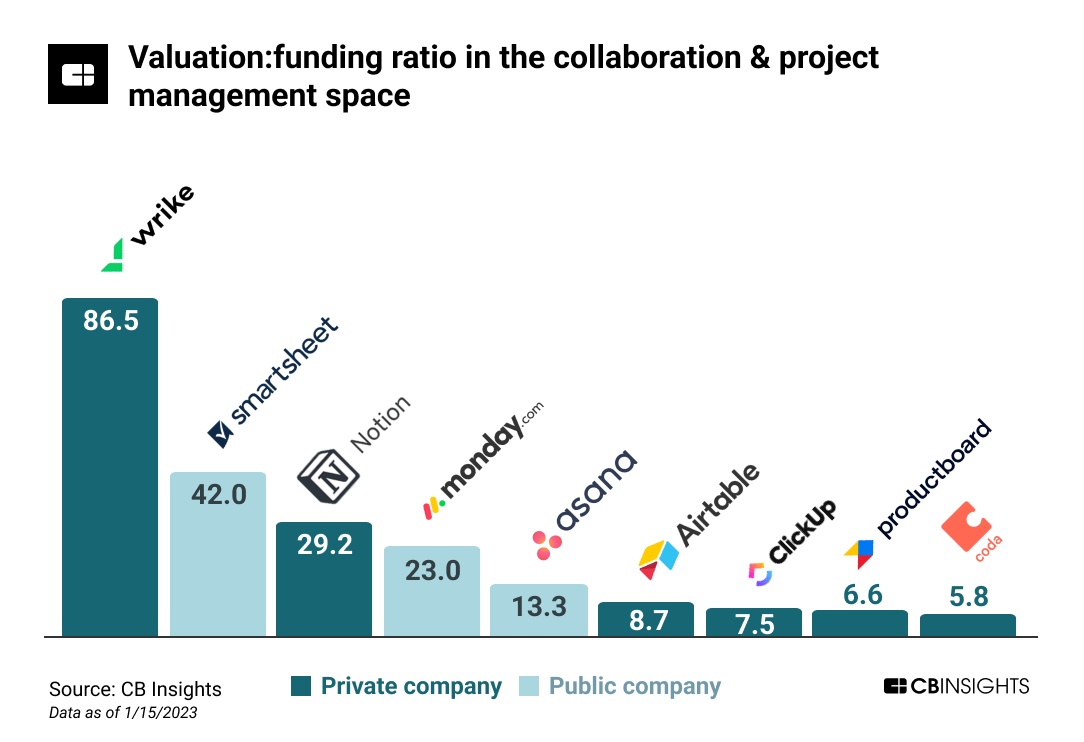

Valuation to funding comparison

- The ratio of valuation to funding (valuation:funding) is a measure of how efficient a company has been in translating funding into value. It also provides a loose proxy for the amount of ownership that a company’s founders and team retain.

- Wrike, which was valued at $2.3B at the time of its acquisition and has raised $26M, has the highest valuation:funding ratio of 86.5. Airtable, which is the most highly valued player in the space as well as the top funded, has a valuation:funding ratio of 8.7.

Want to see more research? Join a demo of the CB Insights platform.

If you’re already a customer, log in here.