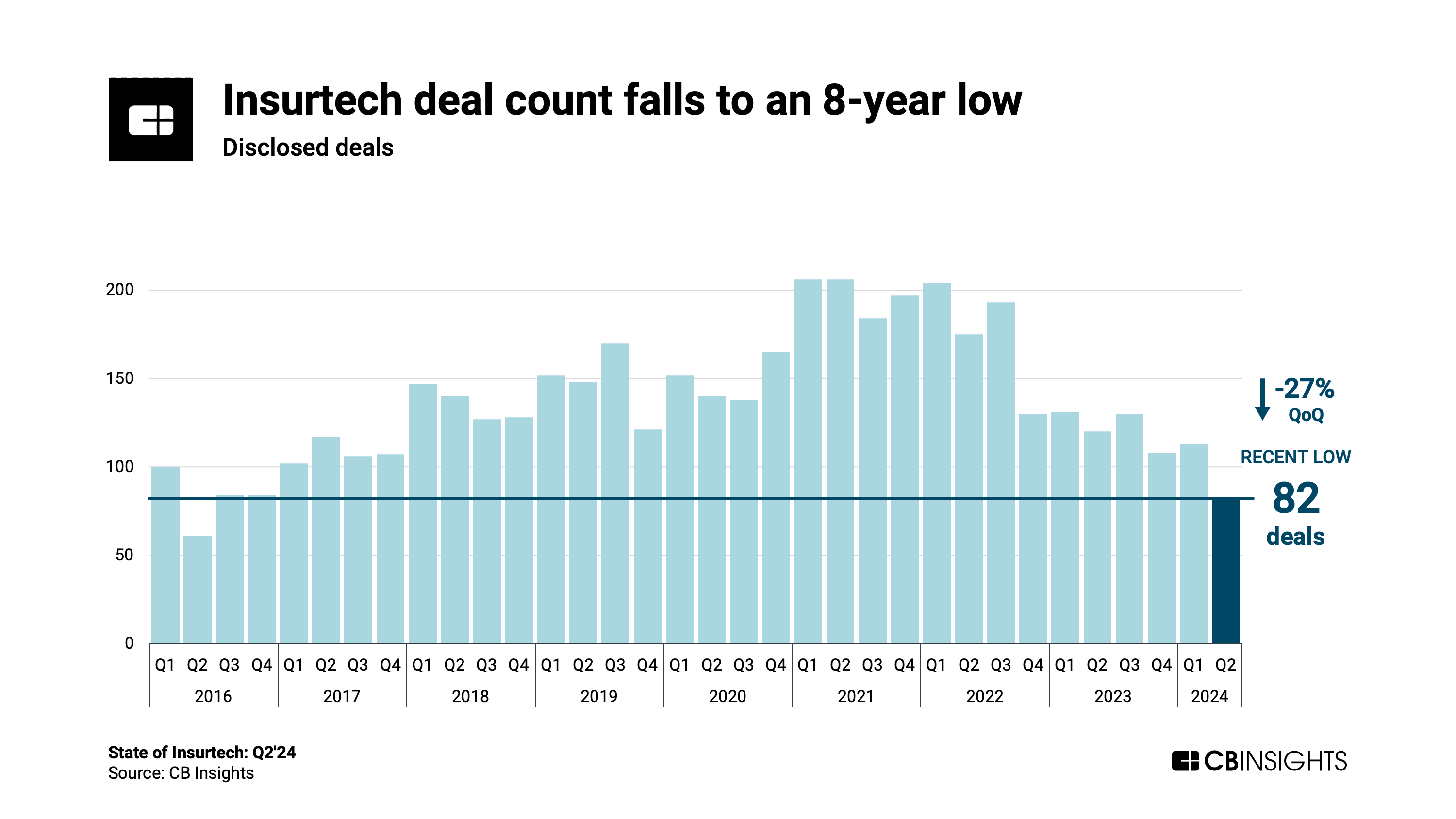

Insurtech funding sees its strongest quarter in over a year despite deal volume sinking to its lowest point since 2016.

Global insurtech funding increased 44% quarter-over-quarter (QoQ) to $1.3B in Q2’24 — outpacing the quarterly growth seen across the broader venture and fintech landscapes.

We provide a deep dive on the state of insurtech in the full report. Here’s the TL;DR:

- Global insurtech funding increases to $1.3B in Q2’24 — the highest level since Q1’23. Insurtech funding grew 44% QoQ — led by 50% growth in funding to P&C insurtechs, from $0.6B to $0.9B. Funding to life & health (L&H) insurtechs also increased QoQ, ticking up from $0.3B to $0.4B.

- Insurtech deal count falls 27% QoQ to 82, the lowest level since 2016. The drop was nearly proportional across P&C and L&H: P&C deals fell 28% to 54 deals, while L&H deals decreased by 26% to 28 deals. On a percentage basis, the decline in insurtech deals outpaced the broader venture and fintech environments (where deal activity fell 7% and 16% QoQ, respectively).

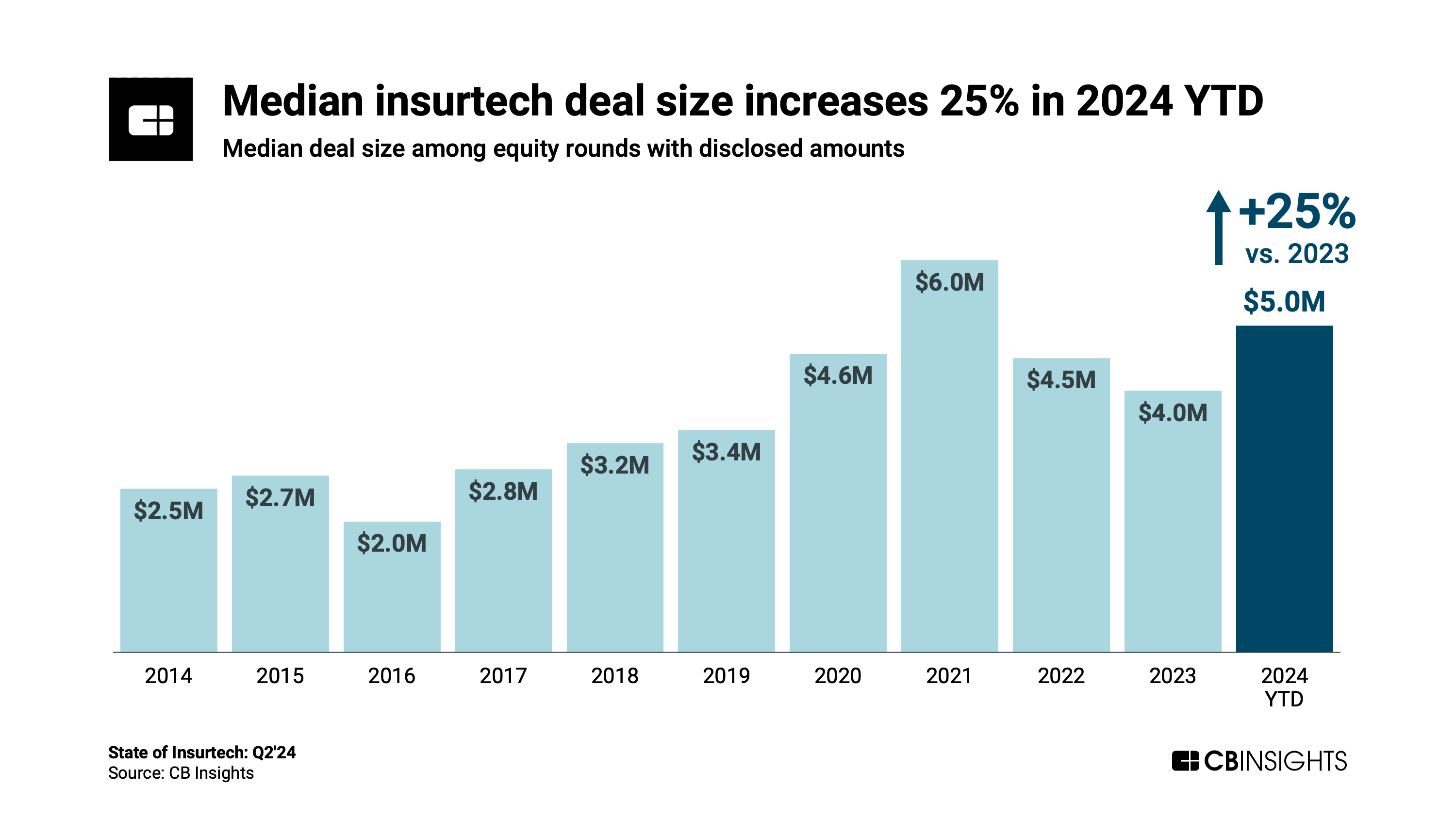

- Median insurtech deal size increases 25% from $4M in 2023 to $5M in 2024 YTD. Only 2021 has seen a higher median deal size over the past 10 years. However, while the median early-stage insurtech deal size is at a record-high $4M this year, late-stage deal size ($31M) is the lowest it’s been since 2018. Insurtech mega-rounds (deals worth $100M+) were nearly nonexistent in Q2, with Sidecar Health, a health insurer, raising the quarter’s only such deal (a $165M Series D).

- Insurtech sees its first IPOs since Q3’22. Two insurtechs IPO’d in Q2’24 — Digit Insurance, an India-based insurance provider, and Saudi Arabia-based Rasan, which primarily focuses on auto insurance sales and vehicle services. Both IPOs occurred amid a broader lull in global IPO activity.

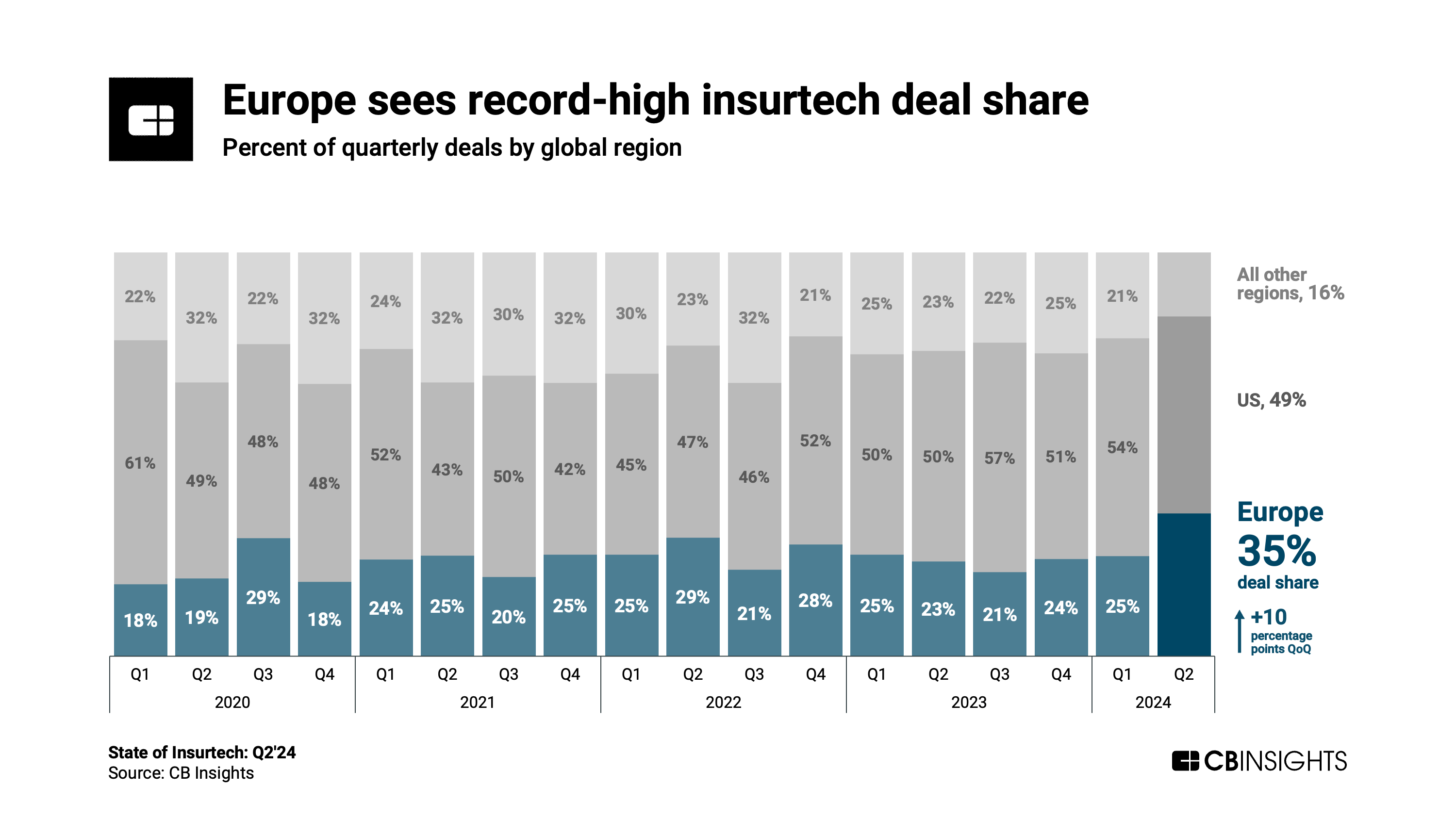

- Europe’s share of insurtech deals reaches 35% — a record high. Deals to Europe-based insurtechs stayed roughly steady, ticking up from 28 in Q1’24 to 29 in Q2’24. Comparatively, the US saw insurtech deal count fall from 61 to 40. Funding to Europe-based insurtechs reached a 7-quarter high ($0.5B), driven by two $93M deals for Finland-based ICEYE — a provider of data from satellite imagery — and UK-based Vitesse, a claims payments processor.