The identity & access management space has seen a wave of consolidation as competition heats up. We break down the IAM landscape across funding trends & exits.

Employees represent one of the greatest cyber risks for businesses. Nearly 75% of cyberattacks involve the element of human error, which includes compromised credentials and privilege abuses, according to Verizon.

To prevent and defend themselves against these security vulnerabilities, enterprises are increasingly adopting identity & access management (IAM) solutions, which ensure that the right individuals have access to the right resources at the right time.

IAM solutions are foundational to a zero-trust cybersecurity framework, where each entity is authenticated before being granted permission to corporate resources. More organizations are moving toward this standard as a proactive security measure. Last year, for instance, the US federal government advised all agencies to adopt a zero-trust model by fiscal year 2024.

Using CB Insights data, we assess the identity & access management landscape across:

- Funding & deal activity

- Exit activity

- Acquisition & take-private valuations

Let’s dive in.

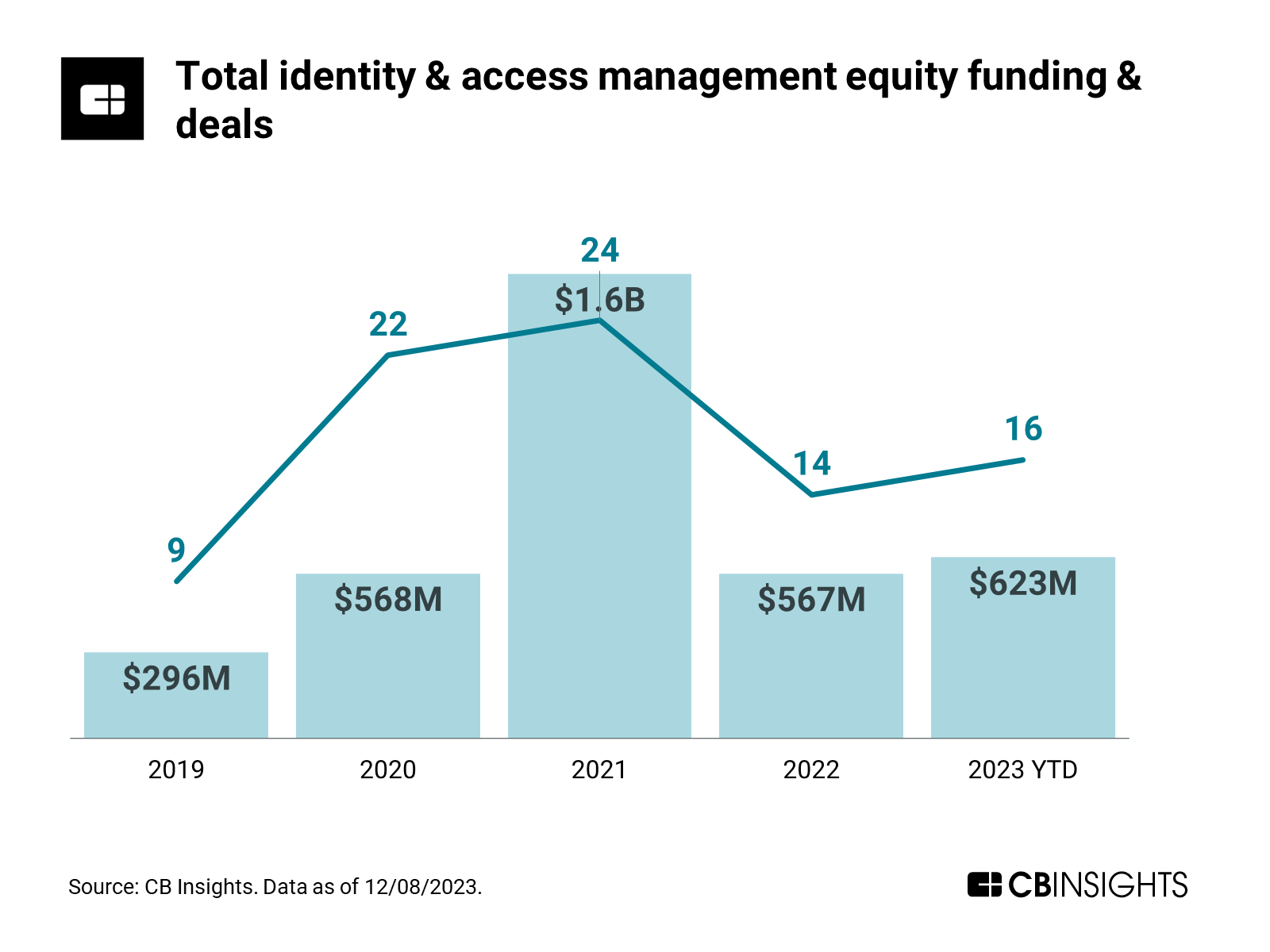

Funding & deal activity

So far in 2023, companies with identity & access management offerings have raised over $600M across 16 deals, outpacing the $567M raised across 14 deals last year.

Employee management platform Rippling’s $500M Series E raise in March is responsible for the majority of funding in 2023, though the uptick in deal activity points to broad interest from a range of investors.

Exit activity

Exit activity has been significant this year — with 4 acquisitions, as well as a SPAC and a take-private transaction — dwarfing previous years’ activity.

Want to see more research? Join a demo of the CB Insights platform.

If you’re already a customer, log in here.