We break down the semiconductor landscape across funding trends, top deals, most valuable companies, and more.

Governments are pouring money into semiconductor development. Since 2022, the US, Europe, and China have each pledged upwards of $40B toward the effort.

There are multiple reasons behind the swelling tide. For one, chips are an integral — and growing — component of devices across sectors, from consumer products to automotive to industrial IoT.

Geopolitics also play a major role. Many countries want to ensure self-sufficiency in an industry they see as being foundational to economic growth and national security.

Massive government investments have helped fuel private-market financing, which surged to a recent high in Q3’23.

Using CB Insights data, we assess the landscape for semiconductors, including:

- Private semiconductor tech firms’ explosive funding quarter

- Public-market industry leaders by market cap

- Which countries dominate private-market semiconductor funding

- The tech startups that raised the biggest equity rounds in Q3’23

- The decline in early-stage deal share in the private markets

Let’s dive in.

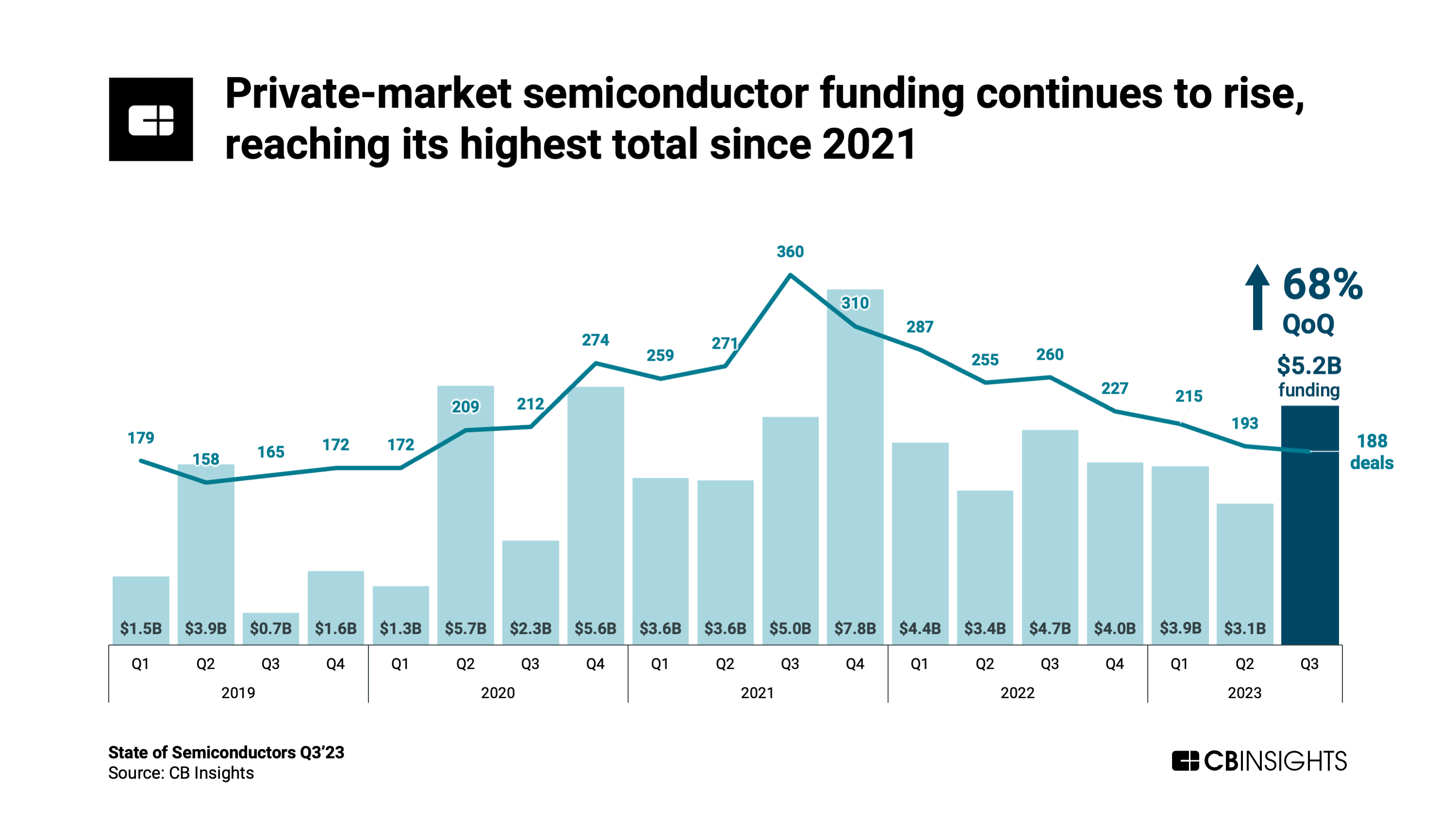

Equity funding to private semiconductor companies increased 68% quarter-over-quarter to $5.2B in Q3’23, marking the highest quarterly funding level since Q4’21, when it reached $7.8B. This is far beyond the growth seen in global venture funding, which increased by 11% QoQ in Q3’23.

Meanwhile, deals continued a steady decline from their peak of 360 in Q3’21 to 188 in Q3’23.

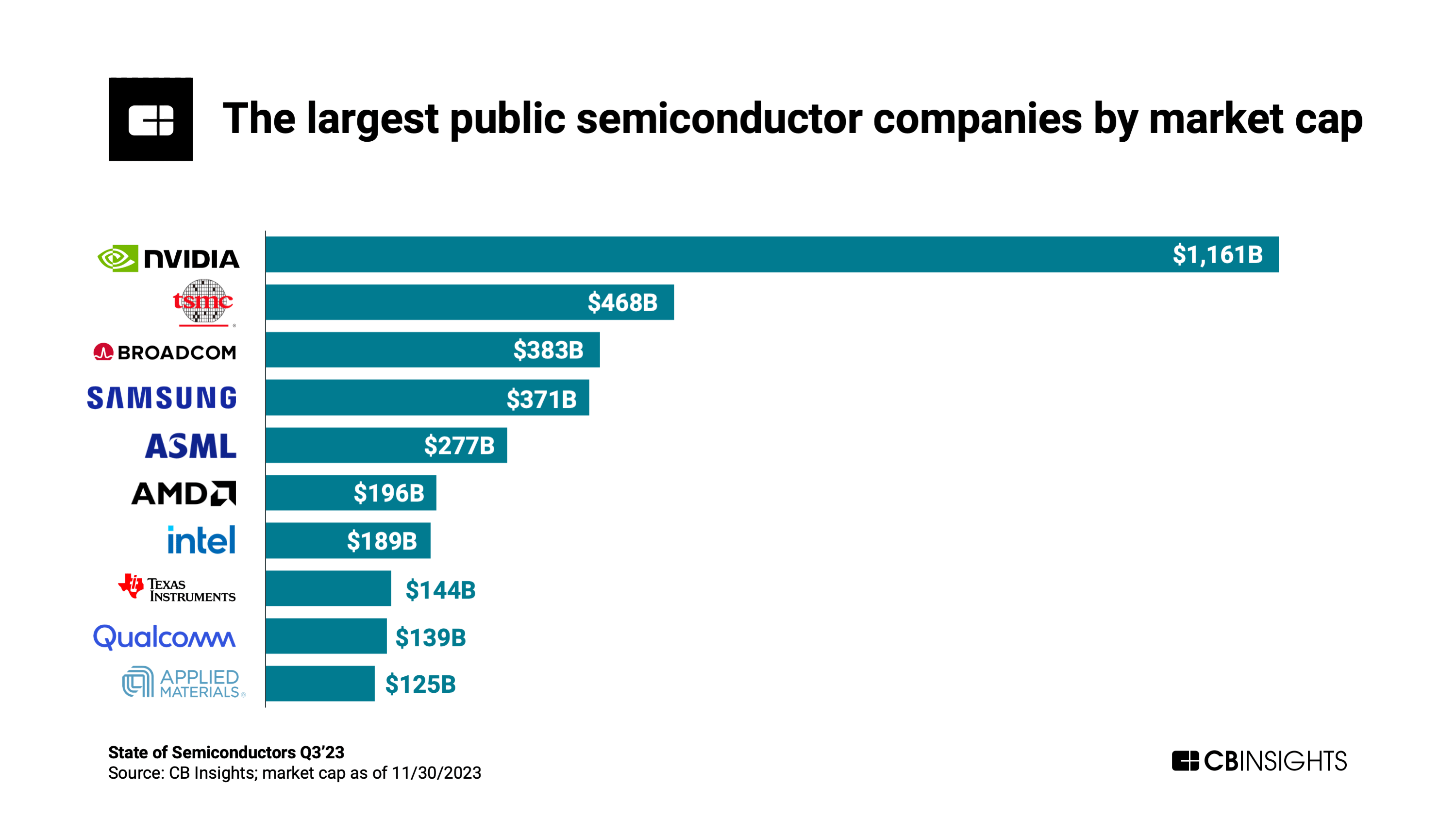

The semiconductor industry is home to some of the largest public-market players in the world, with multiple firms valued over $100B. These firms are primarily located in the US, with a few exceptions (e.g., TSMC in Taiwan and ASML in the Netherlands).

At $1.2T, the highest-valued public player is NVIDIA, whose GPUs are foundational to applications like generative AI.

Want to see more research? Join a demo of the CB Insights platform.

If you’re already a customer, log in here.